PEPSICO (PEP)·Q4 2025 Earnings Summary

PepsiCo Beats Q4, Lifts Dividend for 54th Straight Year

February 3, 2026 · by Fintool AI Agent

PepsiCo reported Q4 2025 results that exceeded Street expectations on both the top and bottom lines, delivering a "sequential acceleration" in revenue growth across North America and International segments. The company affirmed its FY2026 outlook and extended its Dividend King status with a 4% dividend increase—the 54th consecutive annual raise .

Did PepsiCo Beat Earnings?

Yes. Both revenue and EPS came in ahead of consensus:

The GAAP EPS surge (+67% YoY) was inflated by prior-year impairment charges on Tropicana-related investments, making the core EPS comparison more indicative of underlying performance .

Beat Streak: PepsiCo has now beaten EPS estimates in 7 of the last 8 quarters, with the only miss being a narrow $0.01 shortfall in Q1 2025.

How Did the Stock React?

PEP shares rose +1.0% on earnings day, closing at $155.20 . The muted reaction suggests the results were largely in-line with buy-side expectations, with the affirmed (not raised) guidance providing no incremental catalyst.

Context: PEP stock has outperformed in 2026, up ~6% YTD heading into earnings, trading near its 52-week high of $160.15. The stock is now 6% above its 50-day moving average ($146.07) and 10% above its 200-day ($141.62).

What Did Management Guide?

PepsiCo affirmed its December guidance for FY2026—no changes up or down :

Management noted that FX translation is expected to provide a ~1 percentage point tailwind to both revenue and EPS, implying reported net revenue growth of 4-6% and core EPS growth of 5-7% (or 7-9% excluding global minimum tax headwinds) .

Capital Returns: The company announced a new $10B share repurchase program through February 2030, supporting ongoing buybacks of ~$1B annually alongside $7.9B in dividends .

What Changed From Last Quarter?

Several notable improvements relative to Q3 2025:

Key driver: The Beverages North America segment swung from an operating loss in Q4 2024 to meaningful profitability, driven by gains on asset sales, pension liability settlements, and productivity savings—partially offset by tariff-related commodity cost increases (+7 percentage points impact from tariffs) .

Q&A Highlights: What Management Revealed

The earnings call Q&A session provided substantial additional color on PepsiCo's 2026 strategy:

PFNA Affordability Offensive

Management confirmed a major affordability push in Frito-Lay North America:

- Double-digit shelf space gains coming in March/April retail resets—both main aisle and perimeter

- Surgical price investments targeting specific brands, channels, and consumer segments where "the biggest friction for higher penetration is affordability"

- Tested at scale since Q2 2025 with "very good ROI"—volume returns justify the investment

- Frito-Lay expected to grow volume, net revenue, AND operating margin in FY2026

- Growth weighted toward the first half as initiatives take hold

"The average space gain for Frito-Lay in the new resets of both the main aisle and the perimeter will be double-digit." — Ramon Laguarta, CEO

Brand Restaging Playbook

PepsiCo is executing a global restaging of its largest brands in 2026 :

GLP-1 Strategy: "More Opportunities Than Threats"

Management provided a comprehensive response to GLP-1 medication concerns :

- Portion control: 70%+ of food business already in single-serve; investing in capacity

- Hydration: Propel growing 20%+; Gatorade relaunch; powders and tablets

- Fiber: Quaker restaging; SunChips; digestive health focus

- Protein: Ongoing innovation platform

- Cooking methods: Baked, popped, air frying—"multiple technologies"

"There are more opportunities than threats, but they're both. We're approaching this with a sense of urgency." — Ramon Laguarta, CEO

Energy Portfolio: Building to 20% Share

The energy strategy is gaining traction :

- Combined Celsius + Alani Nu portfolio approaching ~20% market share

- Celsius integration showing strong collaboration on execution vs. brand-building split

- Alani Nu rollout not yet complete across all distributors—more acceleration expected

- Energy remains a "fast-growing profit pool" PepsiCo is positioned to capture

Distribution Integration: Texas/Florida Tests

Management confirmed ongoing pilots to merge food and beverage distribution :

- Positive early results on integrated delivery and inventory points

- IT systems and vehicle innovation in progress

- Full update expected "towards the end of the year"

- Solution will not be one-size-fits-all—may include small refranchising in select markets

Acquisition Organic Timing

When acquired brands flip to organic growth :

- Siete: March 2026

- Poppi: July 2026

- Alani Nu: Late 2026

Segment Performance Deep Dive

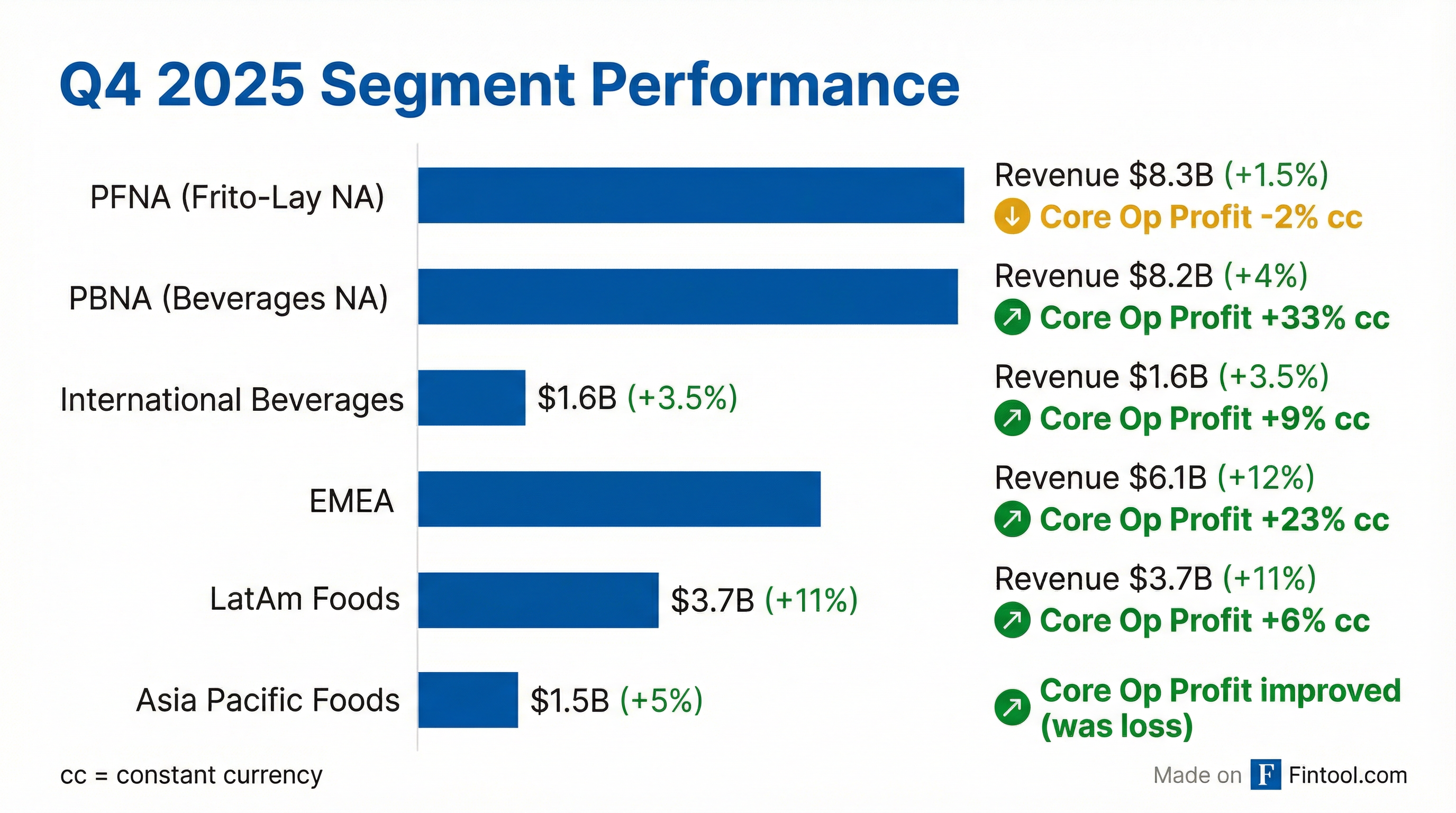

North America (57% of revenue)

Frito-Lay North America (PFNA): Revenue +1.5%, but convenient foods volume declined 1% . Operating profit fell 2% on a core constant currency basis due to higher operating costs, lapping a prior-year gain on Sabra remeasurement, and Quaker recall-related comparisons. Productivity savings partially offset these headwinds.

PepsiCo Beverages North America (PBNA): Revenue +4%, but beverage volume declined 4% . The segment showed dramatic operating profit improvement (+33% cc) driven by favorable prior-year impairment comparisons (Tropicana), asset sale gains, and productivity. However, tariff headwinds (+11 percentage points on commodity costs) and the poppi acquisition integration charges weighed on the quarter .

International (43% of revenue)

EMEA: The standout performer with revenue +12% and core operating profit +23% cc . Strong pricing (+8%) offset volume declines, with productivity savings and favorable FX translation (+14 percentage points) driving margin expansion. Commodity inflation in potatoes, cooking oil, and dairy (+16 percentage points) remains a headwind.

LatAm Foods: Revenue +11%, operating profit +6% cc on effective pricing and productivity . Volume declined 1% as consumers grapple with affordability pressures.

Asia Pacific Foods: Revenue +5%, with volume up 4%—the only region showing positive volume growth . Productivity improvements and lower commodity costs (packaging, potatoes) drove operating profit improvement from a prior-year loss.

Key Management Quotes

"PepsiCo's fourth quarter results reflected a sequential acceleration in reported and organic revenue growth, with improvements in both the North America and International businesses. Accelerated net revenue growth and strong productivity savings led to strong operating margin expansion and double-digit EPS growth in the fourth quarter." — Ramon Laguarta, Chairman & CEO

"For fiscal 2026, we aim to accelerate growth by restaging large, global brands, introducing an expansive set of product innovation in emerging and functional spaces, and offering sharper value to address consumer affordability dynamics. We also aim to deliver a record year of productivity savings which will help fund investments to accelerate growth." — Ramon Laguarta, Chairman & CEO

"We're playing offense here. The investment is manageable for the business. It's included in our guidance. Our productivity progress is going to help fund the initiatives." — Steve Schmitt, CFO (on PFNA affordability investments)

"Families with GLP medication continue to engage in our category, but they do it in smaller portions. The way to keep the category relevant is through smaller portions." — Ramon Laguarta, CEO

Capital Allocation Update

The 4% dividend increase brings the annualized dividend to $5.92 per share (from $5.69), representing a ~3.8% yield at current prices. This marks PepsiCo's 54th consecutive annual dividend increase, extending its status as a Dividend King .

Risks and Concerns to Watch

-

Volume Pressure Persists: Convenient foods volume -1% and beverages -4% in North America highlight ongoing consumer trade-down and competitive pressures .

-

Tariff Exposure: Management called out an 11 percentage point commodity cost headwind in PBNA from tariffs, suggesting vulnerability to trade policy changes .

-

A&M Spend Down $500M+ in 2025: Advertising declined double-digits (~$500M) in 2025 as PepsiCo optimized working and non-working spend. CFO confirmed this benefit will not repeat, and A&M will go back up in 2026—a margin headwind to watch .

-

Rockstar Impairment: The company took a $1.99B impairment on the Rockstar energy drink brand during FY2025, signaling challenges in the energy category .

-

poppi Integration: Acquisition and divestiture-related charges of $453M in FY2025 reflect integration costs from the poppi acquisition, with execution risk ahead .

-

Mountain Dew Turnaround Still Pending: Management acknowledged Mountain Dew has been "a more difficult project" and will "take a little bit longer"—though 2026 is expected to improve vs 2025 .

-

International FX Volatility: While FX is a tailwind for 2026, 28% of revenue comes from emerging markets with inherent currency risk .

Forward Catalysts

- CAGNY Conference: Management noted "see you in CAGNY in a couple of weeks"—expect more detail on 2026 strategic initiatives .

- Lay's Super Bowl Relaunch: Global restaging debuts at Super Bowl with new positioning on freshness and simple ingredients .

- March/April Retail Resets: Double-digit shelf space gains for Frito-Lay go live—key inflection point for volume .

- Siete Organic Flip (March): Siete acquisition enters organic growth, followed by Poppi in July .

- Q1 2026 Earnings: Expected late April 2026. Key focus: North America volume trajectory and affordability investment ROI.

- Distribution Integration Update: Management committed to providing details "towards the end of the year" on Texas/Florida pilots .

- Gatorade/Quaker Relaunches: Major restaging expected in second half of 2026 .

The Bottom Line

PepsiCo delivered a clean beat with sequential improvement in organic growth and strong margin expansion from productivity initiatives. The dividend raise and $10B buyback authorization underscore management's confidence in cash generation.

The earnings call revealed an aggressive 2026 playbook: surgical affordability investments, double-digit shelf space gains, multi-brand restaging (Lay's, Gatorade, Quaker, Tostitos), and a comprehensive GLP-1 response strategy. Management is "playing offense" and expects Frito-Lay to grow volume, revenue, AND margins—a notable confidence statement.

However, with guidance merely affirmed (not raised), A&M spend needing to increase after a $500M cut in 2025, and Mountain Dew still a "difficult project," execution risk remains. The true test comes in March/April when retail resets hit and affordability investments flow through. Watch CAGNY in two weeks for more details.

Related: